Commercial Real estate sales volumes continued to be suppressed through the third quarter of 2024 as we awaited the Federal Open Market Committee meeting on September 18th, during which the Federal Reserve lowered interest rates by 50 basis points. This easing of monetary policy in support of their statutory mandate of promoting maximum employment and stable prices has created optimism in the commercial real estate segment.

Lower interest rates can increase financing activity demand in addition to increasing asset values if net operating incomes remain constant. This demand for financing and resulting transaction activity tends to create liquidity in the debt capital markets. Pencils are being picked back up again as investors think it’s safe and now time to get back in.

That’s great news for that looming $3 trillion of commercial real estate loans that need refinancing.

Commercial Mortgage Maturities by Lender Type ($ Billion)

| Year | Total Due | Banks | CMBS | Life Cos | GSE | Other |

| 2024 | $602.6 | $277.6 | $138.3 | $48.2 | $68.9 | $69.5 |

| 2025 | $598.0 | $286.6 | $112.6 | $50.8 | $82.3 | $65.6 |

| 2026 | $599.2 | $304.5 | $69.6 | $54.4 | $102.3 | $68.3 |

| 2027 | $628.7 | $322.1 | $55.5 | $58.3 | $120.6 | $72.1 |

| 2028 | $620.8 | $320.0 | $56.7 | $60.9 | $114.7 | $68.6 |

| 2029 | $595.1 | $294.0 | $66.7 | $58.1 | $118.1 | $58.2 |

| 2025-2029 | $3,041.8 | $1,527.3 | $361.1 | $282.6 | $538.0 | $332.9 |

Many borrowers were caught when rates increased from 3% to more than 7% in 2022, ending the low-rate environment to which they had become accustomed. But now, with more attractive rates available, borrowers have a renewed interest in refinancing, and we should see investors wanting to take advantage of them.

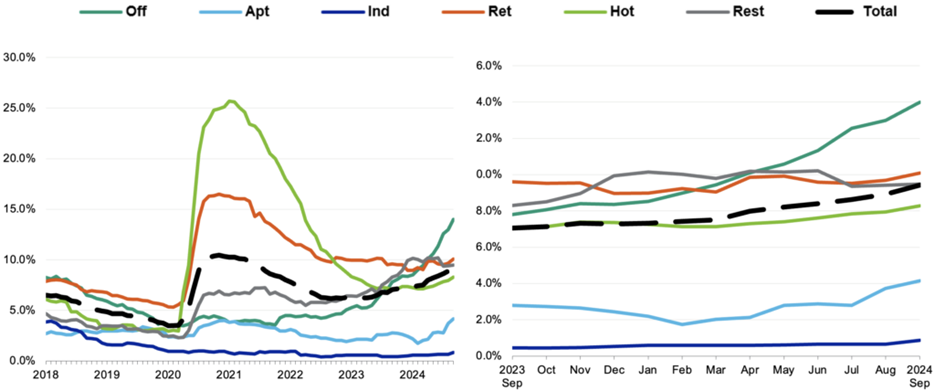

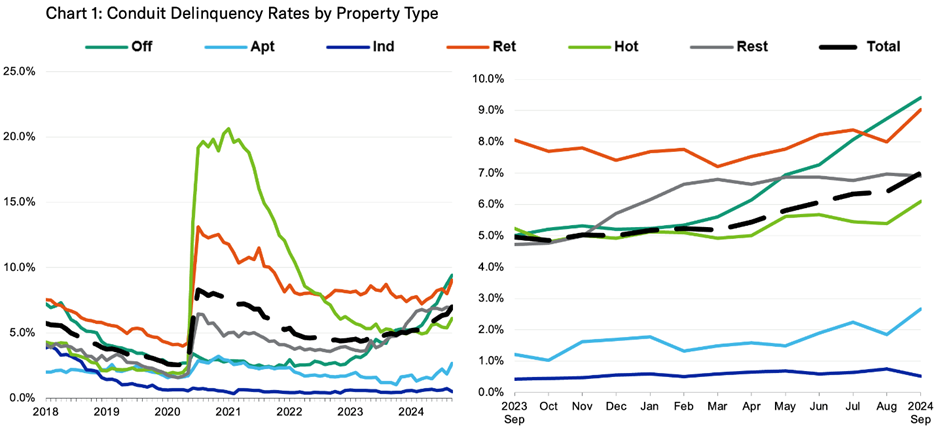

But, not so fast. While there is a good chance that refinance lending will see an increase, many of the outstanding loans still represent distressed assets. A leading indicator of troubled loans is the special servicing rate, which continued its monthly increase from the beginning of 2024 through September. Multifamily, office, and mixed-use segments all saw increases in the special servicing rate in August.

Continuing this trend is the loan delinquencies rate. The total delinquency rate for CMBS loans increased to 7.0% in September 2024. The biggest risk remains within the office segment; however, the retail, hospitality and multifamily segments have all seen increases.

With rates higher than pre-pandemic levels, low valuations and increased concern over some commercial sectors, refinance will remain challenging for some loan types. Many of the largest US lenders have been reducing their exposure within troubled sectors. Additionally, they have prepared for the challenges ahead by maintaining higher loss reserve levels and low loan-to-value rates, providing them with ample equity. We will get through this.

What is the outlook for the remainder of the year? As the Fed continues to pursue its mandate and an elusive “soft landing,” we may see additional rate cuts in 2024. Meanwhile, inflation has fallen, and real wages have grown during the last few years, per the Bureau of Labor Statistics. Unemployment rates are creeping up, but still at historically low rates. And American consumers continue to spend, signaling optimism.

At the same time, substantial liquidity remains on the sidelines, with billions of dollars ready to be deployed. In the remaining months of 2024, we should see increased commercial activity as savvy investors look to maximize their returns.